Car insurance is one of those unavoidable expenses that quietly eats away at your monthly budget. You pay it year after year, often without questioning whether the amount still makes sense. Many drivers assume rising premiums are simply part of life—something you can’t control. But that assumption is costly.

The reality is this: car insurance pricing is flexible, and most people are paying more than they need to. Insurance companies base your premium on dozens of variables—some obvious, others hidden. When you understand these variables, you gain leverage.

This article outlines eight easy and practical routes to cheaper car insurance. These aren’t gimmicks or shortcuts. They are proven strategies that work across income levels, driving experience, and vehicle types. Whether you’re a young professional, a business executive, or managing a family budget, these routes can help you reduce costs without sacrificing protection.

Route #1: Stop Treating Loyalty as a Discount Strategy

The Loyalty Myth

Many drivers stay with the same insurance company for 5, 10, or even 20 years. They believe loyalty will be rewarded with better rates. In reality, insurance companies often do the opposite.

Long-term customers frequently experience:

- Gradual premium increases

- Fewer promotional discounts

- Less competitive pricing

Meanwhile, new customers receive aggressive pricing incentives.

Why Switching Saves Money

Insurance companies constantly adjust risk models. One company may see you as high risk, while another sees you as low risk. Switching insurers allows you to benefit from:

- Introductory pricing

- New customer discounts

- Different risk calculations

Smart Switching Strategy

- Compare quotes at least once a year

- Keep coverage levels identical for fair comparison

- Don’t cancel your old policy until the new one is active

Bottom line: Loyalty rarely equals savings. Comparison does.

Route #2: Adjust Your Deductible With Intention

Understanding the Deductible Trade-Off

Your deductible is the amount you agree to pay out-of-pocket before insurance covers the rest. Lower deductibles mean higher premiums. Higher deductibles mean lower premiums.

Many drivers automatically choose low deductibles without considering:

- Their savings

- Their driving habits

- Their claim history

How a Small Change Makes a Big Difference

Raising your deductible from $250 to $500—or from $500 to $1,000—can reduce premiums significantly, sometimes by 15–30%.

Who Benefits Most

- Drivers with emergency savings

- People with clean driving records

- Those who rarely file claims

Bottom line: A higher deductible, chosen wisely, is one of the fastest ways to lower premiums.

Route #3: Remove Coverage That No Longer Makes Financial Sense

When Full Coverage Is No Longer Worth It

As your car ages, its value drops—but your premiums often don’t. Collision and comprehensive coverage may no longer be cost-effective for older vehicles.

Ask yourself:

- What is my car worth today?

- How much am I paying annually for extra coverage?

- Could I afford to replace the car if needed?

The Math Matters

If your car is worth $3,000 and you’re paying $900 per year for collision coverage, the numbers don’t add up.

Smart Coverage Matching

Insurance should reflect current reality, not past decisions.

Bottom line: Align coverage with vehicle value, not habit.

Route #4: Maximize Discounts Most Drivers Never Ask For

Discounts Are Often Hidden in Plain Sight

Insurance companies offer dozens of discounts—but many are not applied automatically.

Commonly overlooked discounts include:

- Safe driver discounts

- Low-mileage discounts

- Defensive driving courses

- Anti-theft devices

- Multi-policy bundling

- Multi-car households

Why Insurers Don’t Volunteer Discounts

Discounts reduce revenue. If customers don’t ask, insurers often stay silent.

How to Unlock Every Discount

- Call your insurer annually

- Request a full discount review

- Update mileage and driving habits

- Provide proof of safety features or courses

Bottom line: Asking the right questions can instantly lower your bill.

Route #5: Improve Your Credit Score (Even if You’re a Great Driver)

The Credit–Insurance Connection

In many regions, insurers use credit-based insurance scores to predict risk. Statistically, drivers with better credit:

- File fewer claims

- Cost insurers less money

As a result, poor credit often leads to higher premiums—even with a perfect driving record.

How Credit Impacts Your Premium

- Lower credit = higher perceived risk

- Higher credit = better pricing and options

Practical Improvements

- Pay bills on time

- Reduce credit card balances

- Check credit reports for errors

- Avoid unnecessary credit inquiries

Bottom line: Better credit often equals cheaper car insurance.

Route #6: Drive Less—and Make Sure Your Insurer Knows It

Mileage Is a Major Pricing Factor

The more you drive, the higher your risk. Many drivers don’t update their insurer when their mileage drops.

You may qualify for discounts if:

- You work remotely

- You commute less

- You use public transportation

- You own multiple vehicles

Usage-Based Insurance Programs

Telematics programs track:

- Mileage

- Speed

- Braking behavior

- Time of day driving

Safe drivers often receive substantial discounts.

Who Benefits Most

- Remote workers

- Retirees

- City residents

Bottom line: Less driving means less risk—and lower premiums.

Route #7: Be Strategic About Filing Claims

Every Claim Has a Price

Even small claims can result in:

- Higher future premiums

- Loss of claim-free discounts

- Long-term cost increases

Insurance is designed for major financial protection, not minor repairs.

When to Think Twice

- Damage cost is close to your deductible

- The issue is cosmetic

- You’ve filed recent claims

Long-Term Thinking Pays Off

Drivers who file fewer claims often enjoy lower premiums over time.

Bottom line: Not every repair needs an insurance claim.

Route #8: Review Your Policy Every Year Like a Business Contract

Why Annual Reviews Matter

Life changes, and your insurance should change with it:

- New car

- New job

- Marriage or family changes

- Improved driving record

- Better financial position

Yet many drivers keep the same policy for years without review.

Executive-Level Habit

Successful professionals review contracts regularly. Car insurance should be no different.

What to Review

- Coverage limits

- Deductibles

- Discounts

- Competing offers

Bottom line: Annual reviews prevent silent overpayment.

Bonus Tips for Even Cheaper Car Insurance

- Bundle car and home or renters insurance

- Choose vehicles with strong safety ratings

- Avoid coverage gaps at all costs

- Maintain a clean driving record

- Pay premiums annually if discounts apply

Real-Life Example: Saving Without Sacrificing Coverage

James, a mid-level executive, followed these eight routes:

- Switched insurers after comparing quotes

- Raised deductibles strategically

- Removed unnecessary coverage

- Bundled policies

- Improved credit score

- Reduced annual mileage

- Avoided small claims

- Reviewed policy annually

Result: Over 45% savings in three years, with stronger coverage than before.

Conclusion

Car insurance doesn’t have to be expensive. Most drivers overpay simply because they don’t know where to look or what to question.

The 8 Easy Routes Recap:

- Shop around regularly

- Adjust deductibles wisely

- Remove unnecessary coverage

- Ask for every discount

- Improve your credit score

- Drive less and document it

- File claims strategically

- Review your policy annually

When you approach car insurance strategically—like any financial decision—you gain control, reduce costs, and protect your long-term budget.

Summary:

Car insurance is an expense that no driver can avoid, but there are some simple ways to reduce the cost as much as possible. Try these 8 ideas to see how much you could save.

Keywords:

car insurance,auto insurance,motor insurance,cheaper

Article Body:

Car insurance is one of the most expensive costs involved in driving a car, and it’s not something you can avoid – a minimum level of insurance is required by law. That doesn’t mean you have to blindly pay whatever your insurer quotes though, as there are several simple things you can do to reduce the cost of your premiums.

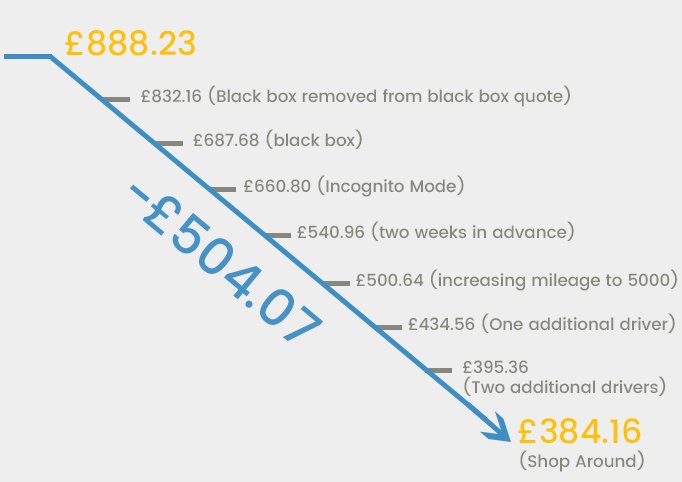

1) Shop around and buy online: Figures show that many people simply renew their current policies without shopping around. The internet makes it easy to compare prices from different insurers, so why not take advantage of this? Plus, you’ll usually get a discount of 10% or more just for buying your policy online.

2) Policy type: do you really need a comprehensive policy with all the extras? Going for a third party fire & theft policy can reduce your premiums hugely, and is definitely worth considering if your car isn’t an expensive model.

3) No claims discounts: Nearly all policies feature a discount that increases for every year you don’t make a claim. The higher the discount available, the more you could save. Also look at insurers offering a ‘no claims bonus for life’ feature, where your current discount level can be fixed forever, even if you have to make a claim somewhere down the line.

4) Excess: The excess on a policy is the amount of a claim you have to pay before the insurer pays the rest. Choosing to have a higher than standard excess level will usually mean lower premiums.

5) Security: Fitting your vehicle with an alarm, immobiliser, or other security devices can lead to premium reductions. Parking you car off-road, for example on a driveway or in a garage, will also mean a cheaper policy.

6) Pay annually: Many insurers charge you interest for the privilege of paying in monthly installments. Pay annually if you can afford it to avoid this, or look for one of the companies who don’t charge extra for monthly payment.

7) Mileage: The more mileage you run up every year, the more your insurance will cost. Even if you can’t reduce your mileage, make sure you’re not overestimating how much you actually do drive, and give your insurer an accurate figure.

8) Drivers: The more drivers you have on your policy, the more it will cost. Reduce the number of people insured to drive your car to the minimum possible, and try to get the policy in the name of a driver with the lowest risk profile. For example, if a car is driven by both a man and a woman, insuring it in the woman’s name will often result in a cheaper quote.

Tinggalkan Balasan