Health care costs continue to rise year after year, placing increasing pressure on individuals, families, and businesses alike. In response to these rising costs, many people are searching for smarter, more flexible ways to manage medical expenses without sacrificing financial stability. One option that has gained significant attention is the Health Savings Account (HSA).

At first glance, HSA plans may seem confusing or even intimidating. They combine health insurance, tax planning, and long-term savings into a single financial tool. However, once understood, HSAs can become one of the most powerful and efficient ways to manage healthcare expenses—both now and in the future.

This article breaks down seven essential things you should know about Health Savings Account plans, explaining how they work, who they are best for, and how they can fit into a broader financial strategy.

Thing #1: An HSA Is More Than Just a Health Account

Understanding the Basics

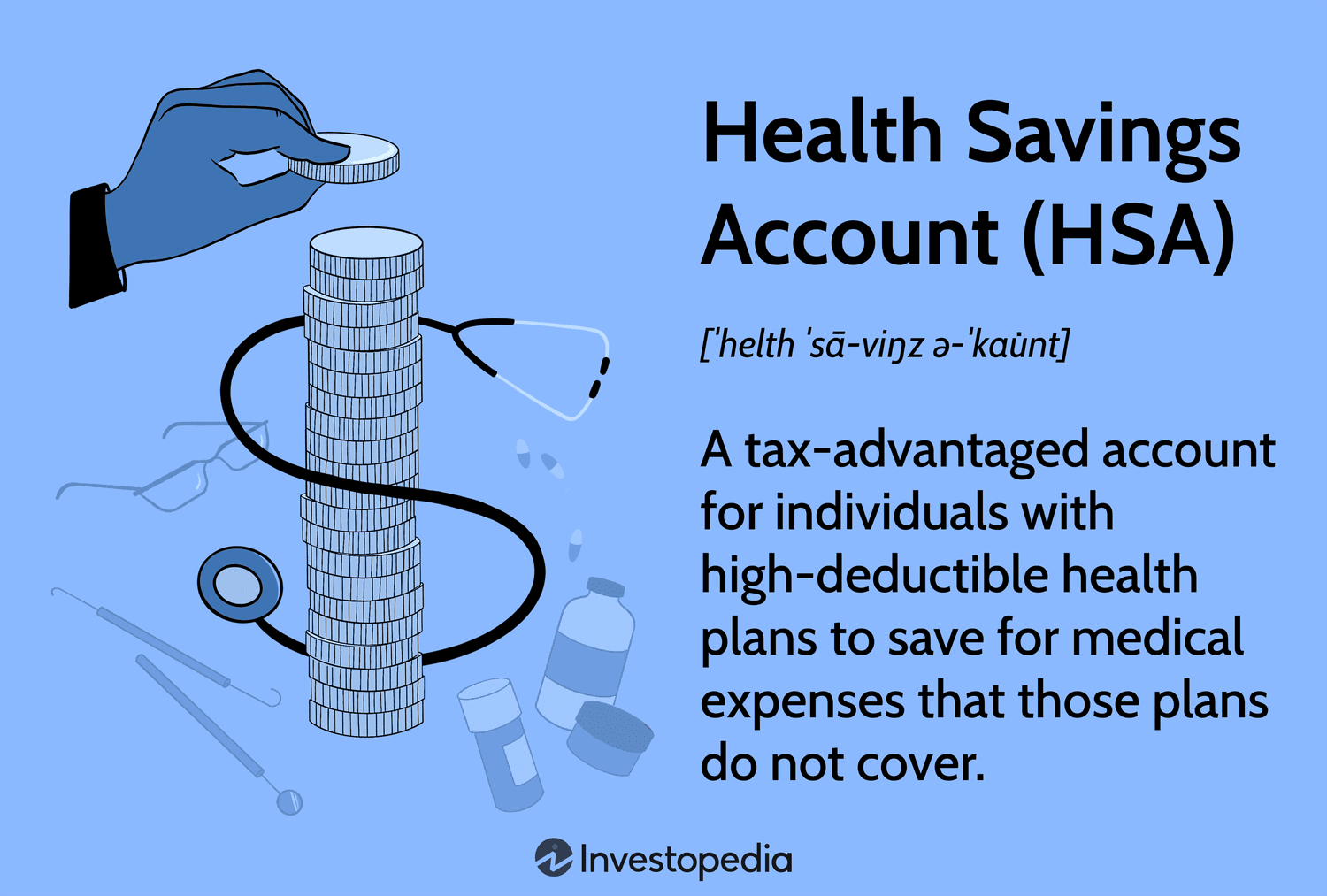

A Health Savings Account is a tax-advantaged savings account designed to help individuals pay for qualified medical expenses. HSAs are only available to people enrolled in a High-Deductible Health Plan (HDHP).

However, many people misunderstand HSAs as being just another checking account for medical bills. In reality, an HSA is a hybrid financial tool that combines:

- Healthcare spending

- Tax savings

- Long-term investment potential

Why This Matters

Unlike Flexible Spending Accounts (FSAs), HSAs:

- Are owned by you, not your employer

- Roll over year after year

- Stay with you even if you change jobs or retire

This makes HSAs uniquely powerful for long-term financial planning.

Big Picture Insight

When used strategically, an HSA can function as:

- A short-term medical expense fund

- A long-term healthcare investment account

- A supplemental retirement savings vehicle

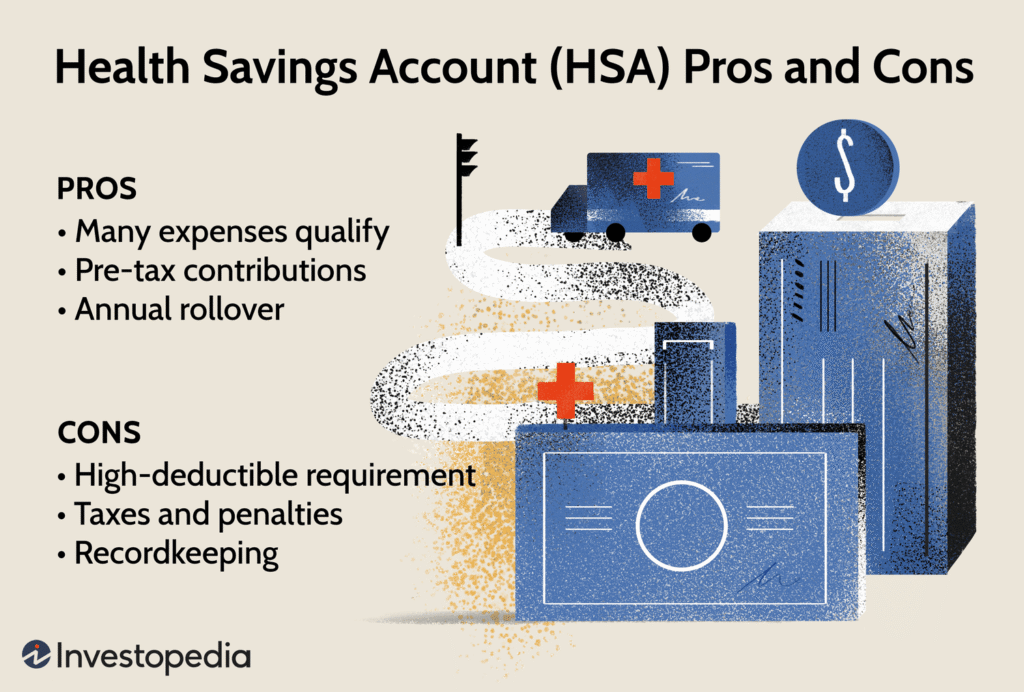

Thing #2: HSAs Offer Triple Tax Advantages

The Triple Tax Benefit Explained

HSAs are one of the very few financial tools that provide three separate tax benefits:

- Tax-Deductible Contributions

Money you contribute reduces your taxable income. - Tax-Free Growth

Interest, dividends, and investment gains grow tax-free. - Tax-Free Withdrawals

Withdrawals used for qualified medical expenses are not taxed.

Why This Is So Powerful

Most retirement accounts only offer one or two tax benefits. For example:

- Traditional retirement accounts are tax-deductible upfront but taxed on withdrawal

- Roth accounts are taxed upfront but tax-free later

HSAs provide tax advantages at every stage, making them one of the most efficient financial vehicles available.

Executive-Level Insight

For high-income professionals, HSAs offer a legal and effective way to reduce taxable income while planning for future healthcare costs—an expense almost everyone will face eventually.

Thing #3: You Must Have a High-Deductible Health Plan (HDHP)

What Qualifies as an HDHP?

To open and contribute to an HSA, you must be enrolled in a qualified High-Deductible Health Plan. These plans typically feature:

- Lower monthly premiums

- Higher deductibles

- Defined out-of-pocket maximums

The exact deductible and out-of-pocket limits are set annually by regulators and vary by coverage type.

The Trade-Off

HDHPs are designed to shift more initial healthcare costs to the consumer in exchange for lower premiums. This structure encourages:

- Cost-conscious healthcare decisions

- Preventive care utilization

- Reduced unnecessary medical spending

Who HDHPs Work Best For

- Healthy individuals with low annual medical expenses

- People with emergency savings

- Those who value lower premiums over predictable co-pays

Thing #4: Your Money Rolls Over Forever

No “Use It or Lose It” Rule

One of the biggest advantages of HSAs is that unused funds roll over indefinitely. Unlike FSAs, there is no deadline to spend your money.

This allows you to:

- Save over many years

- Build a significant healthcare fund

- Plan for major future medical expenses

Long-Term Growth Potential

Many HSA providers allow you to invest funds once your balance reaches a certain threshold. Over time, this can significantly increase the value of your account.

Retirement Perspective

Healthcare costs are one of the largest expenses in retirement. HSAs allow you to:

- Save specifically for future medical needs

- Reduce reliance on retirement income

- Protect other investments from medical-related withdrawals

Thing #5: HSA Funds Can Be Used for More Than You Think

Qualified Medical Expenses

HSA funds can be used tax-free for a wide range of expenses, including:

- Doctor visits and hospital services

- Prescription medications

- Dental and vision care

- Mental health services

- Certain medical equipment

Often Overlooked Expenses

Many people don’t realize HSAs can also cover:

- Physical therapy

- Chiropractic care

- Hearing aids

- Long-term care premiums (with limits)

Strategic Tip

Keeping receipts allows you to reimburse yourself years later, giving you flexibility in how and when you use your HSA funds.

Thing #6: HSAs Become Even More Flexible After Age 65

What Changes at 65?

Once you turn 65:

- You can still use HSA funds tax-free for medical expenses

- You can withdraw funds for non-medical expenses without penalty (though income tax applies)

This effectively turns your HSA into a retirement account with added flexibility.

Medicare and HSAs

You can no longer contribute to an HSA once you enroll in Medicare, but:

- Existing funds remain available

- Withdrawals for Medicare premiums are allowed

Retirement Planning Insight

An HSA can complement traditional retirement accounts by:

- Covering healthcare costs tax-free

- Reducing pressure on taxable retirement income

- Providing flexibility for unexpected medical needs

Thing #7: HSAs Require Strategy, Not Guesswork

Common Mistakes People Make

- Not contributing enough

- Spending HSA funds too quickly

- Failing to invest balances

- Ignoring long-term planning potential

A Smarter Approach

- Maximize contributions when possible

- Pay current medical costs out-of-pocket (if affordable)

- Invest HSA funds for long-term growth

- Save receipts for future reimbursement

CEO-Level Thinking

Treat your HSA as a strategic asset, not just a spending account. With the right approach, it can become one of the most efficient components of your financial plan.

Case Study: Turning an HSA Into a Long-Term Advantage

David, a 42-year-old professional, enrolled in an HDHP and began contributing the maximum amount to his HSA each year. Instead of spending the funds immediately, he:

- Paid routine medical expenses out-of-pocket

- Invested his HSA balance

- Saved receipts for future reimbursement

After 15 years, David accumulated a substantial HSA balance—fully dedicated to future healthcare needs, with tax-free growth.

Conclusion

Health Savings Account plans are often misunderstood, yet they remain one of the most powerful tools available for managing healthcare costs and long-term financial security.

The 7 Key Things to Remember:

- HSAs are more than just health accounts

- They offer triple tax advantages

- An HDHP is required

- Funds roll over indefinitely

- Eligible expenses are broader than most people realize

- HSAs become more flexible after age 65

- Strategic use unlocks maximum value

When used correctly, an HSA is not just a healthcare solution—it is a smart financial strategy for the future.

Summary:

A health savings account plan offers lower premiums and lower taxes for many individuals. Before switching to an HSA plan, however, one would be well advised to seek the counsel of an experienced benefits specialist who is familiar with insurance companies offering high deductible policies that qualify for HSA account participation. In some situations, the lower costs anticipated may not be realized, or may not be worth trade-offs necessary to achieve those savings.

Keywords:

employee health savings account, flexible health savings account, health care savings account, health savings account, health savings account plan, health savings account tax

Article Body:

Health savings accounts (HSAs) are wildly popular. Since their introduction in 2004, approximately 2.5 million Americans have enrolled in these so-called consumer-driven health plans. But, alas, HSA plans are not for everyone.

Here are some pointers to help you consider whether an HSA will benefit you and your family.

- An HSA plan can cut healthcare costs by an average of 40% for many people.

Nevertheless, some people will not realize any net savings. Those most likely to realize significant savings are people who pay all of their own health insurance premiums, such as the self-employed, who are relatively healthy with few medical expenses. - health savings plan restores freedom of choice.

An HSA plan puts individual consumers back in control of their own health care. This also means that each individual must be more responsible for his or her own health care decisions. This approach of self-reliance is not always popular with or appropriate for everyone, especially those who have become comfortable with HMO-type “co-pay” plans. - Health savings accounts reduce income taxes.

Every dollar contributed into your HSA account is deducted from your taxable income in the same manner as contributions into a traditional IRA account–regardless of whether you spend it or just save it. Interest and investment earnings in a HSA accumulate tax-deferred, just like a traditional IRA. Unlike an IRA, withdrawals are tax-FREE when used to pay qualifying medical expenses. In many situations, new account holders are able to almost fully fund their HSA with money saved on premiums from a prior, higher priced plan. By stashing all or most of those savings into an HSA, the account holder realizes instant, additional savings in the form of reduced taxes. - You must have a properly qualified high health insurance policy in place first before

you can open a health savings account. One of the biggest misconceptions about HSA plans is that any insurance policy with a high deductible will qualify the policyholder to establish an HSA account. IRS regulations, however, are quite specific. Not just any policy with a so-called “high deductible” will suffice. It is important to be certain that you are insured under a properly qualified policy. Your best bet is to work with a qualified and duly licensed health insurance broker who is experienced in marketing properly qualified HSA plans. - You must be insurable in order to qualify for the HSA-qualified health insurance policy.

Because most people do not have a properly qualified high deductible insurance policy, they will need to switch insurance plans in order to become HSA-eligible. Unless coverage is being offered under small group reform laws (generally groups with 2-49 employees), the new high deductible policy will be individually underwritten by an insurance company. This means that some “pre-existing” conditions may not be fully covered. Alternatively, some companies may opt to cover certain “pre-existing” conditions in exchange for slightly higher premiums. Unfortunately, some health conditions simply render an individual uninsurable (examples: diabetes, chron’s disease, heart attack, etc.). Underwriting requirements vary by state, which is another reason to rely on an experienced health plan broker.

You should not switch to a HSA plan when the management of existing medical expenses is more important than saving up-front medical insurance premiums. Do not change health plans: in the middle of ongoing medical treatments; after a major health issue has been diagnosed; or if any family member is pregnant.

Generally, it is relatively hassle-free to qualify, i.e. no medical exams, etc. Most insurance companies offering HSA coverage will issue based on your application answers, perhaps accompanied by a follow-up telephone interview. In some cases, medical records may be requested, and companies always reserve the right to order a paramed exam. - Although HSA insurance premiums are low, they are not always as low as you might expect.

This happens for one main reason. Simply stated, the underlying insurance policy is just that�a health insurance policy. Although it has a “high” deductible, as required by law, the insurance company still must compensate for the risk it is assuming over the deductible amount, which it does by charging premiums. Many companies offer policies with �one deductible� that all family members contribute toward. With those plans, it is not uncommon for premiums for a 5000 family deductible with 100% coverage after the deductible to be comparable to a 2500 “per person” deductible plan with 80/20 coverage after the deductible.

Lower premiums represent just one element of the lower net cost achieved with an HSA plan. The low net cost of an HSA plan is achieved after factoring in the benefits of lower taxes, made possible by the tax-deductible contribution to the HSA account. Thus, if obtaining the lowest possible gross premium is your main concern, you may wish to consider a high deductible, non-HSA policy, especially if you do not see the benefit to contributing to a tax-deductible savings account. - An HSA offers your best chance to keep a lid on health insurance rate increases.

Make no mistake-you will have rate increases with your HSA insurance policy. Because an HSA qualified policy is still a health insurance policy at heart, there is no logical reason to presuppose that an HSA policy would be immune to rate increases required by an insurer to keep paying claims and stay in business. But what you can expect is that the actual dollar amount of any future rate increases will be substantially lower compared to traditional health insurance plans (regular PPO and HMO plans). This is true because insurers base increases on percentages, and the same percentage of a lower base premium results in a lower dollar increase. It’s not a perfect solution-but it is the most cost-efficient solution for many qualified people.

Tinggalkan Balasan